.png)

Many employers don’t realize how much pharmacy benefit manager (PBM) practices affect company costs and your employees.

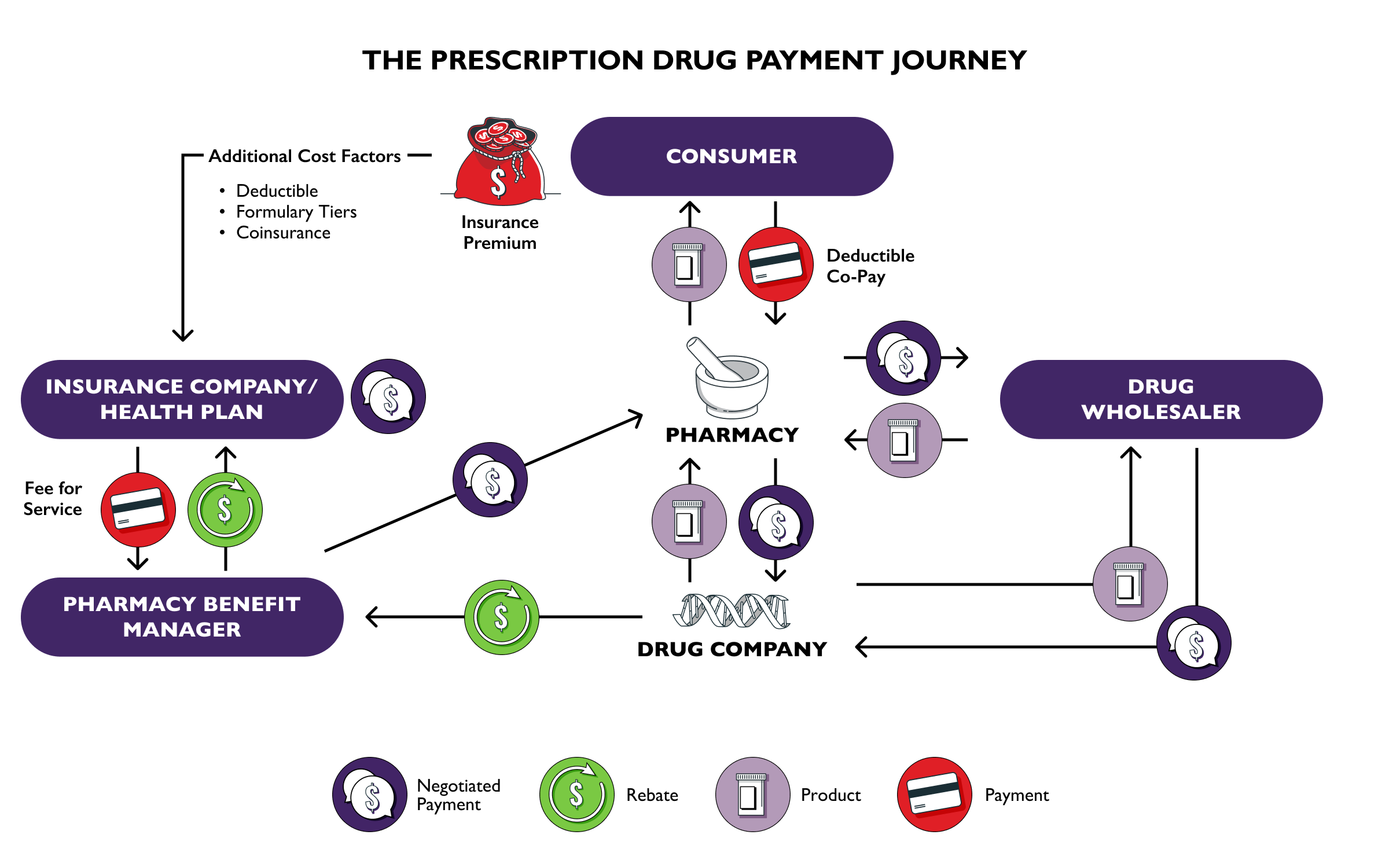

A rebate is a financial kickback from the drug manufacturer to the PBMs for putting their drug on your formulary.

When PBMs negotiate large manufacturer rebates, they usually pocket some of these savings and pass the rest onto the insurer or self-insured employer. Rebates and discounts are rarely passed on to patients. This practice artificially drives up drug prices and leaves patients paying significantly higher out-of-pocket costs.

The average rebate on a brand name drug is ~50%, meaning patients pay double what the insurance plan pays for the drug. Passing rebates through improves adherence and lowers long-term care costs—with minimal impact on overall plan budgets. Expensive complications from unmanaged chronic conditions are the real drivers of plan costs.

Ensure the employees on your health plan have access to lower-cost medications and protect your company from potential litigation.

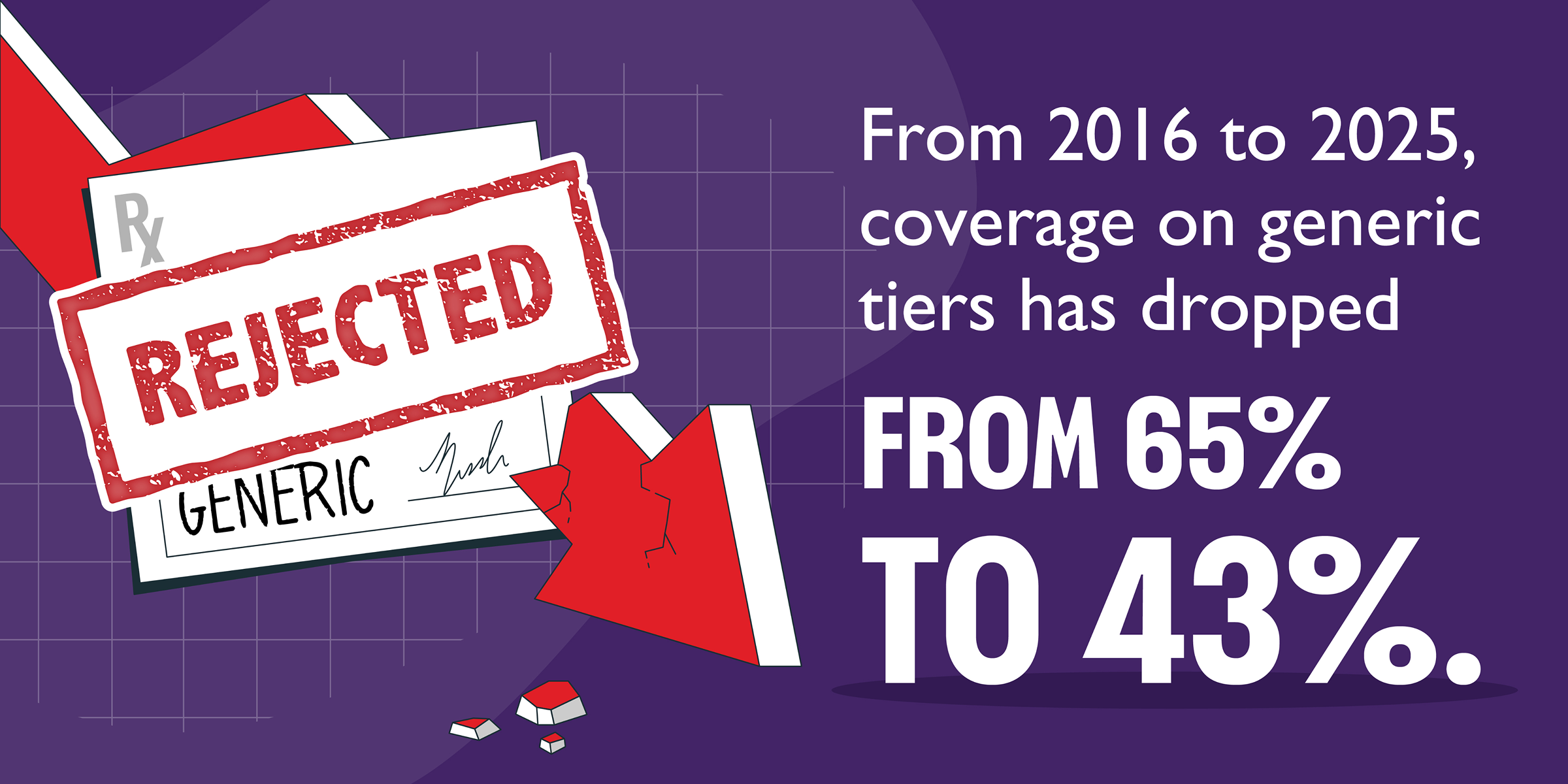

Generics and biosimilars are often blocked from plan formularies despite their substantially lower cost. When they do make it on formulary less than half of generics and biosimilars are placed in the generic tier by PBMs.

Why? PBMs have a perverse incentive to keep higher priced drugs on formularies due to the sizable rebates that are generated by branded drugs. PBMs keep a portion of these rebates and drive participants to the highest price drug not the lowest cost drug.

Investigate this practice in your health plan. Denying participants access to lower-cost options especially during the deductible period, not only reduces adherence and raises plan costs, but can expose you and your company to legal liability.

Tying PBM compensation to drug prices drives up costs for you and the employees on your health plan

When compensation is based on a percentage of the list price, PBMs have little incentive to prefer lower-cost drugs. Delinking breaks the link between PBM profits and the price of a drug—encouraging cost-effective prescribing, reducing wasteful spending, and improving transparency. Employers can fix this broken system by demanding to pay a flat service fee in their PBM contracts.

Patients deserve a say in the medications and devices they rely on. Plan formularies should prioritize clinical value—not just cost. PBMs often change drug coverage based on rebates, not what's best for disease management, disrupting care and driving up short and long-term costs.

When patients are forced to change medications for financial—not medical—reasons. This practice disrupts patient care and exposes plans to unintended costs and risk.

PBMs update their formularies often, sometimes two or more times per year. This practice is called non-medical switching, where patients are switched from current, effective medications to higher rebate alternatives, purely for the PBM’s profitability. Non-medical switching may cause disease complications, leading to costly emergency room visits, lab testing, and extra doctor appointments—increasing health plan costs and worsening patient health. The only winner here is the PBM.

Lower plan costs and improve health outcomes by negotiating health plans that grandfather in effective medications for participants.

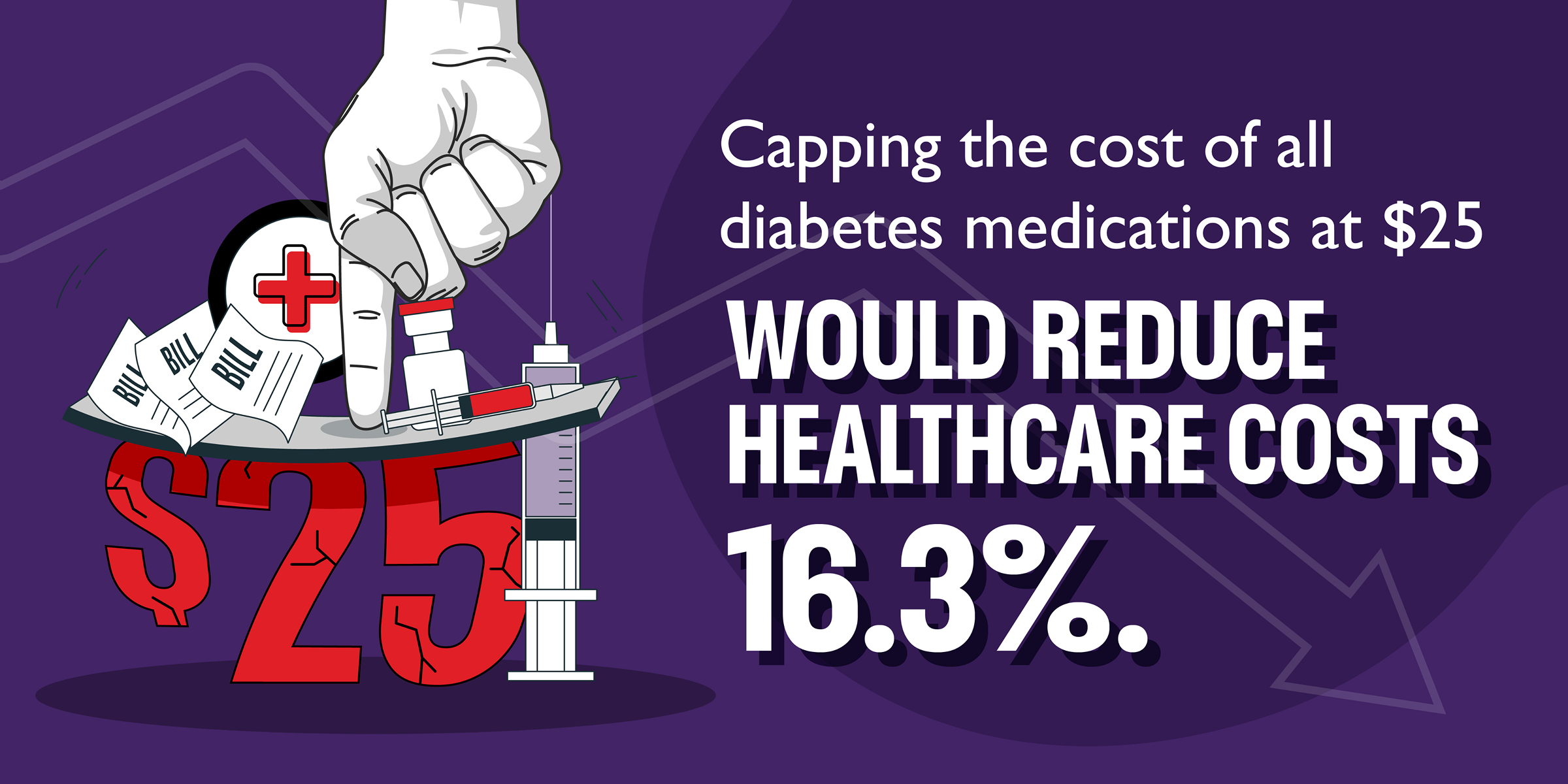

One size doesn’t fit all—especially in diabetes care.

From insulin pumps to continuous glucose monitors (CGMs) to automated insulin delivery (AID) systems, the right tools can dramatically improve outcomes and lower overall health costs. But what works for one person may not work for another. Devices aren’t always compatible, and user interfaces can vary greatly. The best diabetes device is the one the patient can and will actually use.

When participants are limited to a single “preferred” device based on your health plan, outcomes suffer. As one patient put it, “not everybody drives a Ford.” Plans should cover the full range of clinically effective diabetes technologies to ensure choice, functionality, and better adherence.

Diabetes medications need to be affordable because adherence is key. First-dollar coverage is a smart investment.

Without first-dollar coverage for diabetes management tools—like CGMs and insulin—patients often ration their medications and device usage leading to expensive ER visits and long-term complications, including heart and kidney disease.

Yet, many employers still choose health plans that limit access and prioritize short-term savings over long-term outcomes. Early, uninterrupted access starts with exempting diabetes management from the deductibles in your plan.

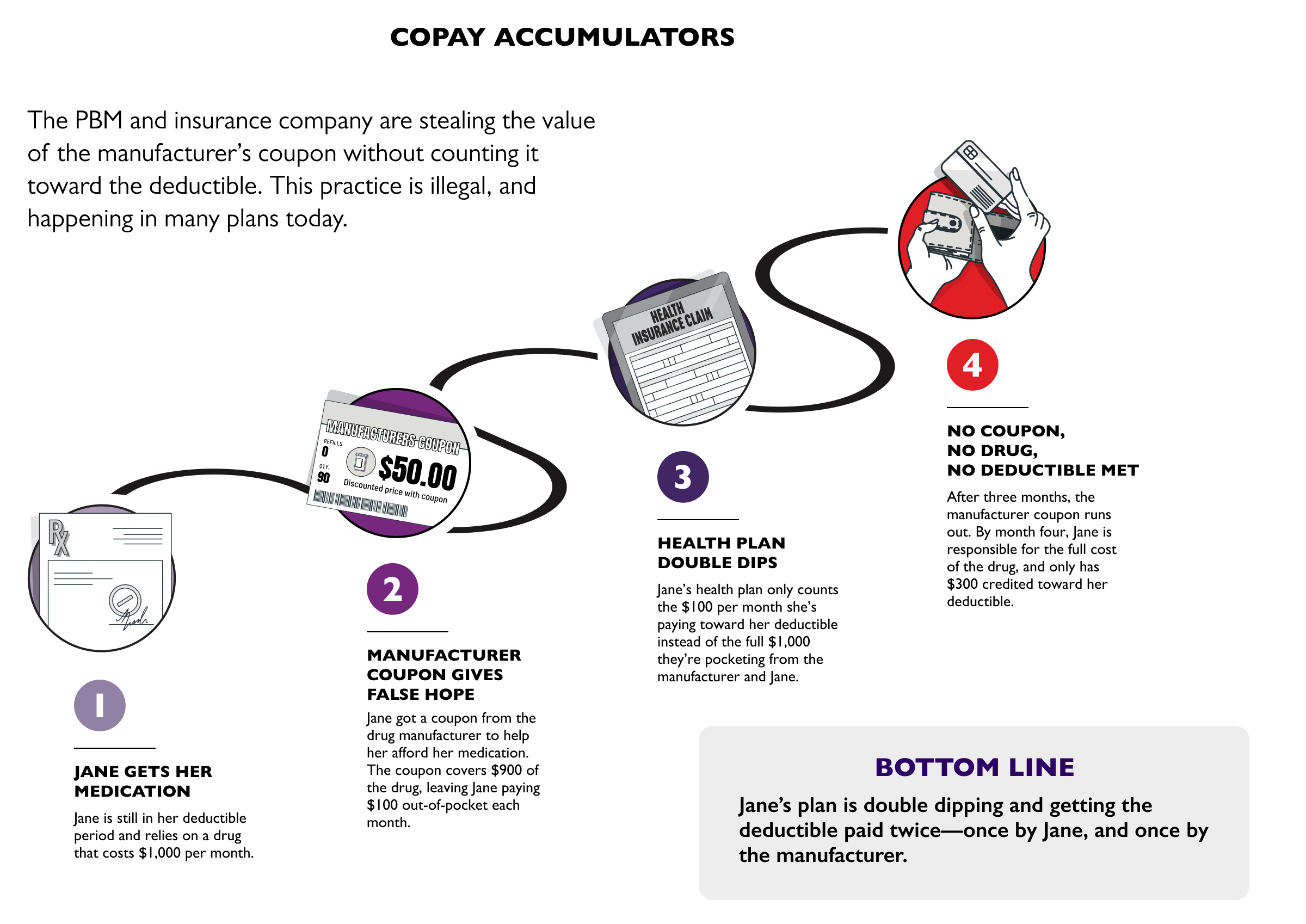

Patients with chronic or rare conditions often rely on manufacturer copay assistance to afford costly medications. But accumulator and maximizer programs increasingly undermine that support—without most employers realizing it.

Copay Accumulators: A patient uses a manufacturer coupon during their deductible period. The pharmacy accepts it—but the plan doesn’t count it toward the deductible. When the coupon runs out, the patient still owes the full deductible and often can’t afford the drug. The result is that the deductible gets paid twice—once by the manufacturer, once by the patient. This practice is illegal in ERISA plans but still common—make sure it’s not in yours.

Copay Maximizers: The drug is dropped from the formulary and falsely deemed non-essential. The employee is pushed to a third party to access it through the manufacturer’s program. The patients’ cost does not count toward their deductible or out-of-pocket max—and the “enrollment” often forces them to lie or hand over financial records and power of attorney. Not a good look for any employer trying to build trust.

Utilization management techniques are intended to lower the cost of your health plan. Ironically, these “savings” strategies can increase overall costs through avoidable complications, nonadherence, and poor patient experience. Employers should examine whether these policies are truly saving money—or just shifting costs and causing harm.

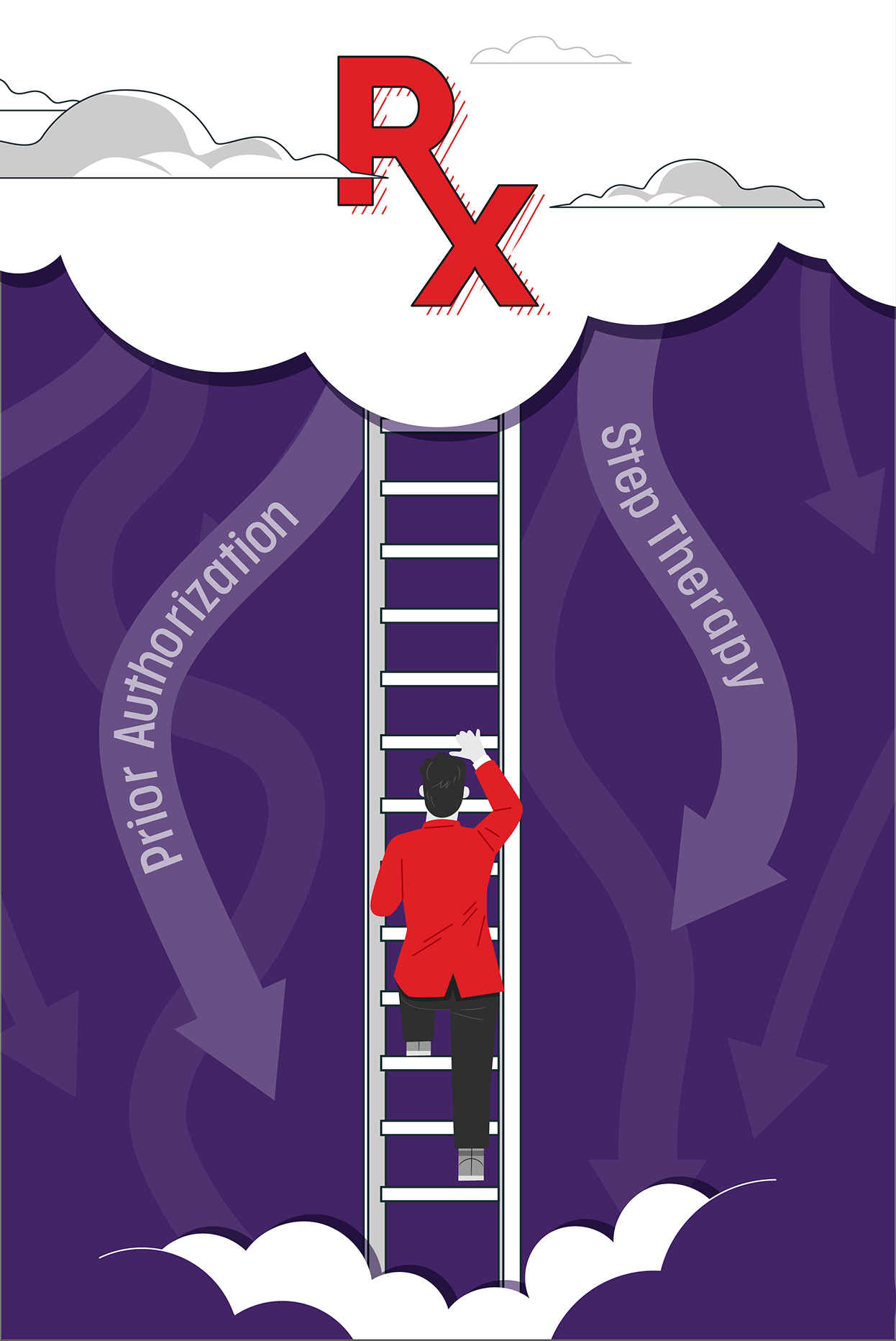

Delayed care is not managed care.

Too often, prior authorization requirements delay access to essential medications—even for long-standing, stable therapies or simple dose changes ordered by a physician.

According to a 2024 survey by the American Medical Association, 89% of physicians said “prior authorization somewhat or significantly increases physician burnout”, largely due to the 39 prior authorization requests that each physician completes each week on average.

These repetitive hurdles frustrate employees, drain provider time, and create barriers to care with no clinical benefit.

Partners like the Regulatory Relief Coalition, along with bipartisan lawmakers, are pushing legislation to streamline and standardize prior authorization—especially for chronic conditions. Employers can support these efforts by reviewing plan policies and prioritizing smarter, faster access to proven treatments.

Disrupted care is not managed care.

Also known as “fail first,” step therapy requires patients to try—and fail—on a lower-cost drug before the plan will cover the one their doctor originally prescribed. In many cases, the patient has already tried that drug and knows it doesn’t work.

While the trial medication may be less expensive, the consequences disrupt patient care and often lead to disease complications. This practice is extremely frustrating to both employees and their doctors. Consider building in common sense waivers for patients who have been on the lower medication before, perhaps on a prior plan. Also, waive this practice during pregnancies where there is not time to jump through multiple hurdles. The lowest cost baby is the one delivered without complications.

.png)

Employers have other opportunities to rein in hidden costs and protect patient choice. These tactics can improve transparency, strengthen local care, and ensure plan dollars go where they matter most—toward better health outcomes.

Spread pricing is a hidden markup—paid by you.

This term refers to the deceptive practice when a PBM charges the plan one price for a drug, pays the pharmacy a much lower price, and keeps the “spread,” or difference.

States like Louisiana, Michigan, and Ohio, are pursing legal action to ban this practice due to the prevalence and rising costs of prescription drugs. Some states have passed legislation and sued for millions of dollars to protect local pharmacies and patients, yet PBMs continue to actively decry this reform.

Ban spread pricing in your PBM contract to increase transparency and ensure plan dollars go to care, not middlemen.

Communities pay the price when choice is limited.

The top three PBMs are part of vertically integrated corporations that control over 80% of the market and profit from steering your employees to their own pharmacies—often by mail order. This frustrating tactic limits choice, adds inconvenience, and drives up costs for you and your plan’s participants.

Even worse, these covert practices contribute to the closure of independent and rural pharmacies, breaking ties to trusted community care and reducing access for patients who depend on in-person support.

.png)

.png)

.png)